We all know that person who isn’t much fun to be around, but you see said person everyday at work, and he or she may occasionally offer to grab you a coffee, or they sometimes give you solid advice about the local area. So when the time comes that you’re having a party, you consider inviting them, because you don’t want them to feel left out if another coworker you’ve invited brings it up. Awkward! You know that person. Wait, are you that person? We kid, we kid! Anyway, that person is kind of like the VA Funding Fee. Stick with us here…

At Hawaii VA Loans, we’ll be the first to tell you that there’s no FUN in a fee. However, you may be pleasantly surprised to learn about some of the VA Funding Fee’s attributes – like how it can be paid, exemptions on VA funding fees, and the VA funding fee refund – so at least it can be deemed invitable, even if it’s not going to increase the fun factor that the VA home loan party is already having!

Triple F: VA Funding Fee Facts

- Fact #1: The VA Funding Fee payment goes directly to the VA and helps to reduce costs of the VA Home Loan Guaranty program to taxpayers.

- Fact #2: The funding fee amount is based on a veteran’s military category (Regular Military, Reserves or National Guard) and the type of loan (purchase loan, refinance loan, etc).

- Fact #3: Back in 2020, it was announced that Hawaii’s VA Loan Limit would be NO LIMIT! This change came about as a result of the Blue Water Navy Vietnam Veterans Act of 2019. In order to fund the program, Congress needs a revenue source, so the additional revenue from increased VA funding fees will go to support the costs.

Read the official details of the “No Limit” announcement here: https://www.benefits.va.gov/homeloans/documents/circulars/26_19_23.pdf

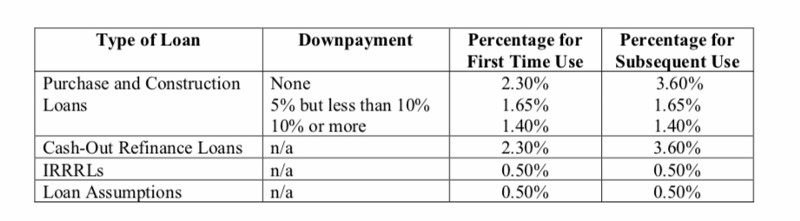

Take a look at the *new* VA Funding Fee Table to find out how to calculate VA loan funding fees:

- The VA has increased the VA funding fee by .15% (previously 2.15%) for all purchase and cash-out refinance transactions.

- The old 0.25% increased funding fee for veterans who earned their eligibility through National Guard/Reserves service has been eliminated. The fee will be the same regardless of how the entitlement was earned.

- There is a new funding fee exemption for active duty service members who have received a Purple Heart.

When & How is the VA Funding Fee Paid?

The VA Funding Fee is a payment made at loan closing (otherwise known as a closing cost) by a veteran or servicemember who uses their VA benefits to finance their home purchase. The fee can be paid by cash OR it can be financed (rolled into the loan).

Exemptions on VA Funding Fees

There are servicemembers and veterans who can receive exemptions from the VA Funding Fee.

The exemptions include:

- Veteran receiving VA compensation for a service-connected disability, OR

- Veteran who would be entitled to receive compensation for a service-connected disability if you did not receive retirement or active duty pay, OR

- Surviving spouse of a Veteran who died in service or from a service-connected disability.

VA loan borrowers who are exempt from paying the funding fee will have their exemption indicated in their Certificate of Eligibility (COE).

VA Funding Fee Refund

What happens if a disability rating is given to a veteran after loan closing? Can a veteran get a refund after closing? Yes, if the disability rating is confirmed by the VA and meets their requirements as to eligibility (the veteran is entitled to disability income retroactively to a date before loan closing), a veteran can be eligible for a refund.

To begin, once the veteran receives their disability rating, he or she should use their current mortgage statement to reach out to their lender and their local VA office for guidance on obtaining a retroactive VA Funding Fee refund.

Here’s an example of how the refund process will work:

- After receiving a VA disability compensation, the veteran requests to have their Certificate of Eligibility (COE) updated. The veteran’s mortgage lender can help do this with the required documentation (ie: VA disability award letter, DD-214, etc.)

- Once the COE has been updated to reflect the correct VA disability rating, the COE and refund request needs to be submitted by the veteran’s lender to the VA Department.

- After submission, the veteran’s current lender will work with the VA Department for verification and apply a one-time principal reduction payment (lowering your loan balance) in the amount of the originally charged VA Funding Fee at the time of loan.

*Please note that the veteran will be the initiator of notifying an updated disability status to their loan service provider.

Now that you’ve learned more about the VA Funding Fee, are you ready to join the VA home loan party and become a Hawaii homeowner? VA loans in Oahu and all Hawaiian islands are easy and simple when you choose Hawaii VA Loans for your VA financing! Contact us to get started.