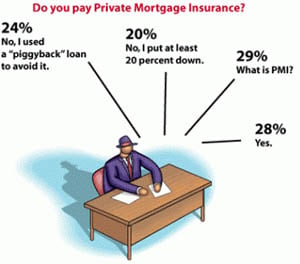

There have been a lot of changes in the mortgage industry lately. Some of the most recent changes have been in the Mortgage Insurance (MI) industry. Private mortgage insurance is a type of insurance used by lenders to help limit losses in the event of loss or foreclosure of a loan. Lenders typically require MI for loans in which there is less than a 20% down payment (for purchases) or equity (for refinances). The mortgage insurance company will absorb losses up to a certain percentage of the value of the loan.

There have been a lot of changes in the mortgage industry lately. Some of the most recent changes have been in the Mortgage Insurance (MI) industry. Private mortgage insurance is a type of insurance used by lenders to help limit losses in the event of loss or foreclosure of a loan. Lenders typically require MI for loans in which there is less than a 20% down payment (for purchases) or equity (for refinances). The mortgage insurance company will absorb losses up to a certain percentage of the value of the loan.

For example, if someone wants to buy a house and has a 10% down payment, a lender will provide a loan of up to 90% of the value of the home. Because there is less than a 20% down payment, the lender will require MI to cover losses equivalent to 25% of the loan amount. This insurance for the lender is a fee that borrowers pay monthly with their loan payment.

A little over a year ago, the mortgage insurance companies began consolidating. Some went out of business altogether, while others joined forces. There are now only about 1/3rd the number of mortgage insurance companies surviving. Over the past 12 months, they began restricting their guidelines and changing pricing to better reflect the associate risk.

Recently, they have discontinued providing mortgage insurance for investment properties and cash out transactions. They also began restricting insurance availability for condos and ‘soft market’ areas in counties for which property values are declining. In Hawaii, despite Fannie Mae or Freddie Mac’s ability to purchase low down payment loans, there are no mortgage insurance companies remaining who will provide insurance for properties with less than 10% down. Many MI companies have also discontinued providing mortgage insurance for loans originated by a mortgage broker, they will only insure loans originated by the lender itself.

The great thing about the VA loan program is that the insurance or ‘guarantee’ is provided by the VA department itself. The VA has not changed their requirements and the VA program continues to offer 100% financing for single family homes and approved condos without a monthly mortgage insurance ($200-$350 savings per month). None of the aforementioned MI changes affect the VA loan process and the VA loan program continues to gain strength and favor in our current real estate market